A Brief MLP Primer

An MLP is a publicly traded entity that is listed on the major U.S. stock exchanges and conforms to the same accounting, reporting and regulations as any publicly traded corporation. MLPs are significant owners of America’s energy infrastructure, controlling substantial assets involved in the transportation, processing and storage of the nation’s energy resources. These assets include major pipeline systems that deliver products such as natural gas, crude oil and refined fuels to end markets. Subsequently, nearly all other critical infrastructure is directly dependent upon the products that MLPs deliver.

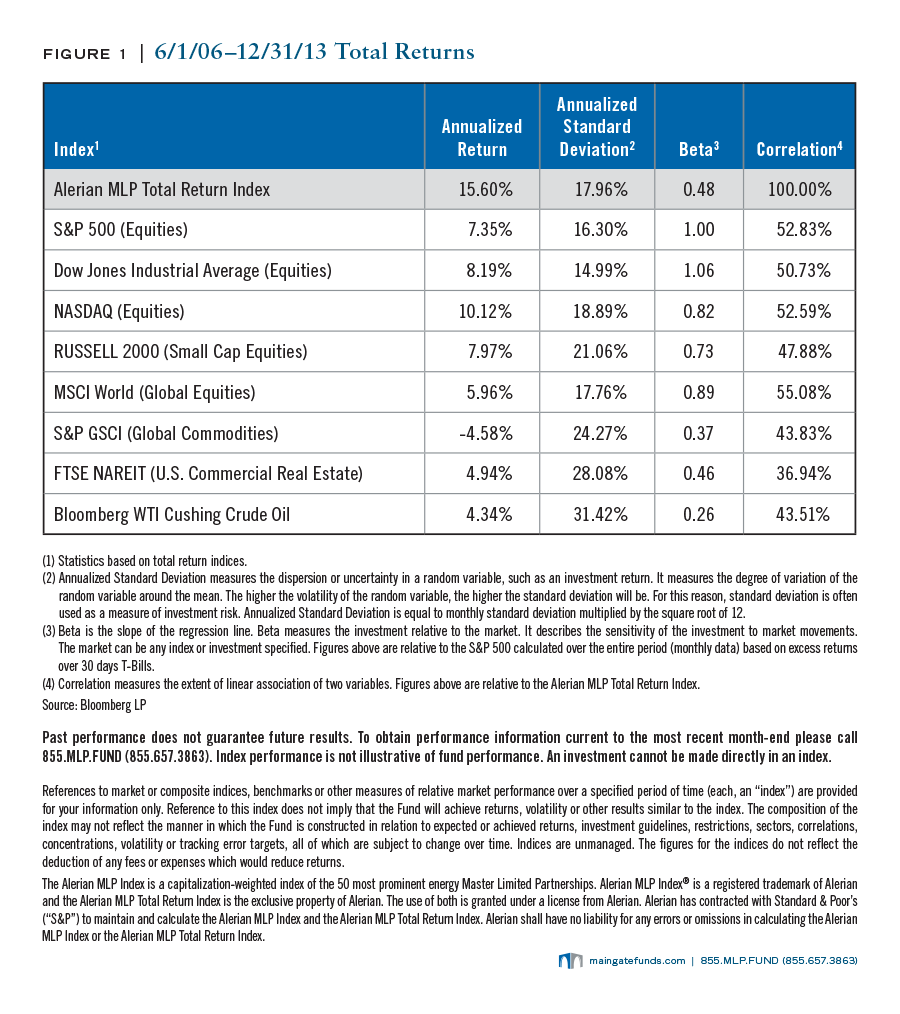

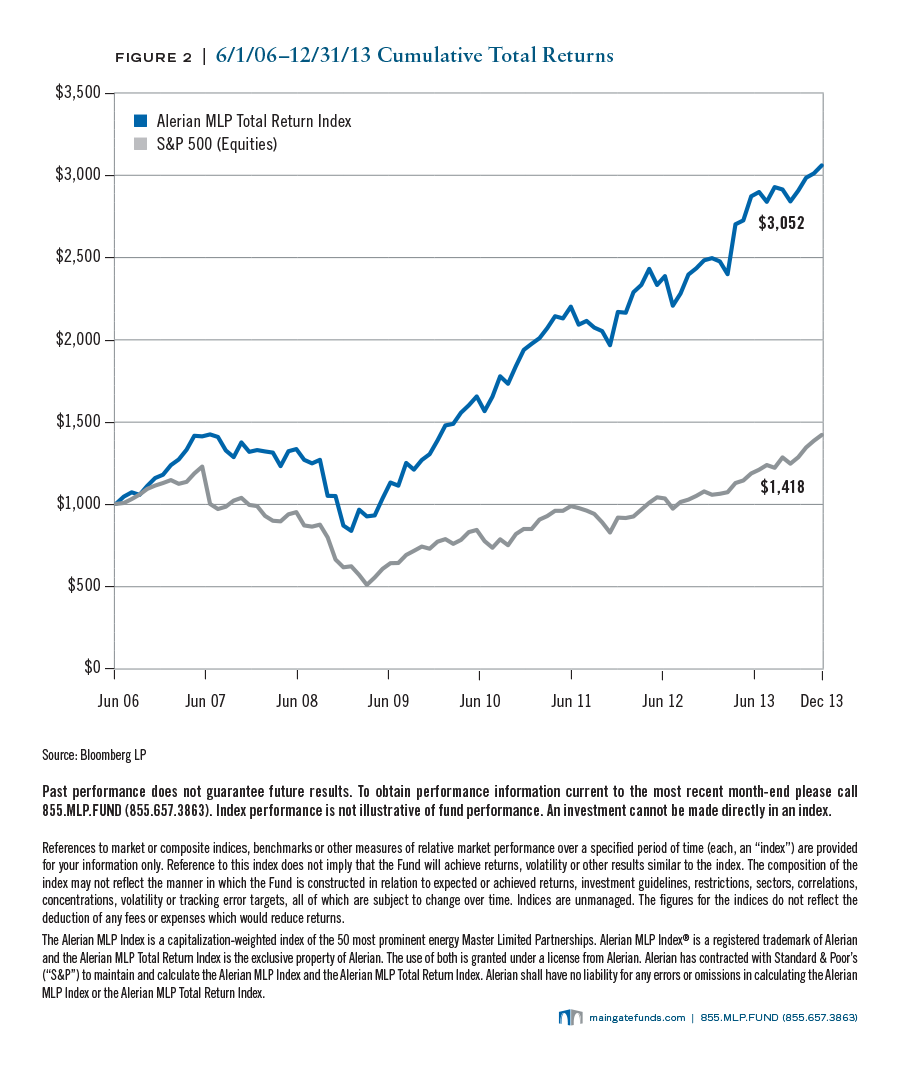

MLPs offer many important attributes that make them a compelling infrastructure investment class. First, they have historically exhibited strong performance compared to the broader equity markets, with lower risk and lower correlation to other asset classes (see Figures MLP 1, 2). Second, MLPs pay quarterly cash distributions, providing the potential for attractive current yields. Typically, these distributions have been relatively stable and predictable because MLP business models have been dominated by fee-based, tariff-oriented revenues from businesses that are supported by inelastic U.S. energy demand. Lastly, MLPs offer the liquidity and flexibility of being publicly traded.

{kind=link}

{kind=link}

An MLP may be organized as either a limited partnership or a limited liability company. It enjoys the tax treatment of a partnership in which all tax items, including depreciation, pass fully to the unit holders through an annual Schedule K-1. Due to this partnership tax status, MLP investors avoid the double taxation experienced by shareholders of regular corporations. A partnership that does not generate 90% or more of its gross income from qualifying sources is treated as a corporation for tax purposes.

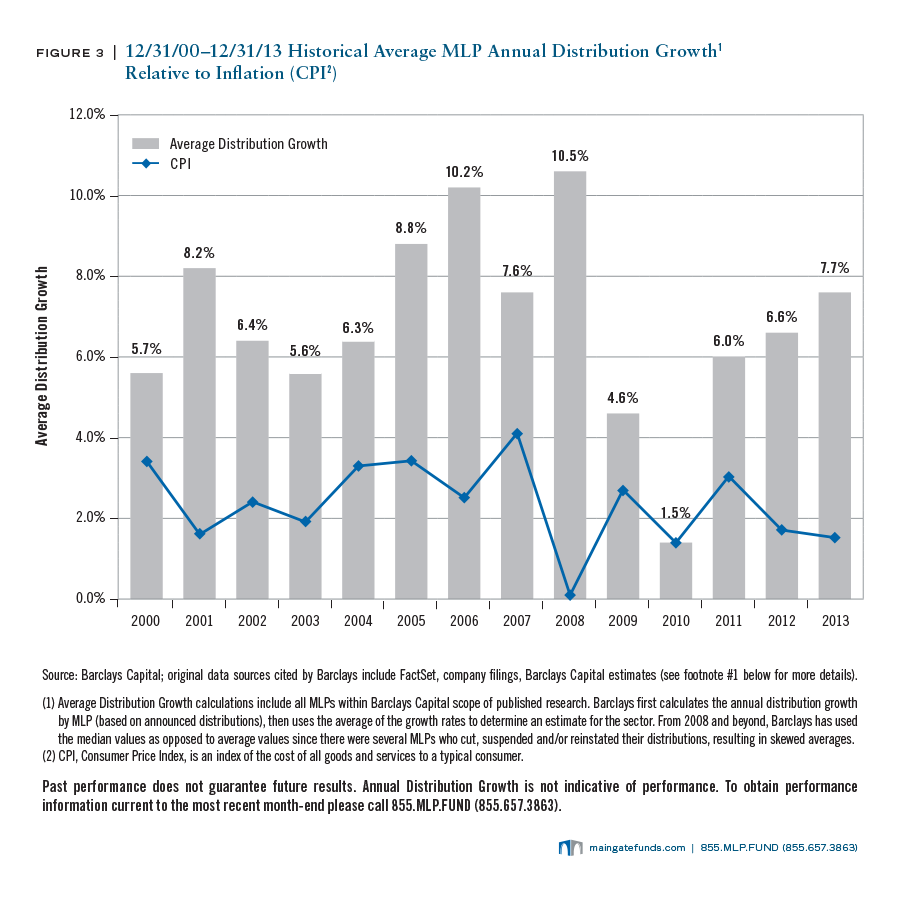

The strong returns that many MLP investors have historically enjoyed are based on two primary factors — yield and growth. MLPs have consistently traded in the public market with distribution yields that average almost 6% over the last thirteen years (see Figures MLP 3). Through modest growth in energy demand, along with an attractive rate structure, MLPs delivered an average growth of 4-8% annually during the period 1998-2008 (Source: Wachovia Capital Markets, LLC, MLP Primer – Third Edition, 2008).

{kind=link}

MLPs appear well positioned to grow due to their significant participation in the build-out and consolidation of the U.S. energy infrastructure — an infrastructure that is forecast to require hundreds of billions of dollars in new development over the next decade. MLPs are also a likely buyer of many midstream energy infrastructure assets currently owned in both private and public corporate entities. Additionally, the MLP market is poised to potentially receive vast additional assets in new forms of energy infrastructure introduced by technological advancements. These assets include liquefied natural gas terminals, gas-to-liquids technology, bio-fuel assets, renewable energy assets, and coal gasification projects.

Midstream energy MLPs bear a close resemblance to a toll-road business model as most do not take ownership of the commodities transported and thus are minimally influenced by fluctuations in commodity prices. Many midstream MLPs receive a capacity reservation fee paid by a local utility or directly from the shipper in order to guarantee product delivery, which minimizes their dependency on volume. This type of contract should provide stable cash flow and help limit the MLP's credit risk as commodity prices fluctuate.

MLPs have the potential to provide a valuable inflation hedge within an infrastructure portfolio in three distinct ways. First, as mentioned above, by having market rates for both tariff and non-tariff assets tied to government reported inflation measures such as PPI (Producer Price Index) and CPI (Consumer Price Index), cash flows are not diluted in an inflationary world. Infrastructure assets also traditionally hedge inflation through the rising replacement cost of long-lived hard assets and/or Gross Domestic Product (GDP) growth associated with increased asset use. Lastly, MLPs involved in businesses such as propane, heating oil, exploration & production, coal and certain gathering & processing activities have typically displayed more seasonal and commodity sensitivity associated with their cash flows. Inflation hedging capabilities can be expanded by increasing one's portfolio allocation toward MLPs involved with these more commodity sensitive businesses.

In addition to certain MLPs that possess commodity price exposure, all energy oriented MLPs are subject to energy risks. Changes in end-user demand or innovative energy alternatives could affect the need for transportation, processing and storage through the existing infrastructure owned by MLPs. Lower commodity prices affect certain MLPs in two ways: Firstly, lower commodity prices may negatively affect production, which could impact future MLP growth projects. Secondly, for those gathering and processing MLPs with equity volumes in their contracts, lower commodity prices on natural gas and natural gas liquids could lead to lower margins. For those MLPs with equity volume sensitivity, it is important to maintain effective and detailed hedging programs to help preserve cash flow and distributions.

MLPs have demonstrated a variety of compelling characteristics, balanced with modest risk in our view, over a long time period. MLPs may offer an attractive investment opportunity that should be considered as a potential core holding within any investor's asset allocation.

__________

Any tax or legal information provided is merely a summary of our understanding and interpretation of some of the current income tax regulations and is not exhaustive. Investors must consult their tax advisor or legal counsel for advice and information concerning their particular situation. Neither the Fund nor any of its representatives may give legal or tax advice.